Relevant Documents:Voluntary PetitionFirst Day AffidavitDIP Financing Motion13 Week Cash ForecastLuca International Group, a Houston-based explorer and producer of natural gas, petroleum and related hydrocarbons, and several affiliates filed bankruptcy petitions

on Thursday in the Southern District of Texas listing $50 million to $100 million in assets and $50 million to $100 million in liabilities. The case number is 15-34221 (DRJ). The case has been assigned to Judge David Jones in Houston.

Luca attributes the bankruptcy filing to insufficient cash flow to cover operational expenses. In addition, the company points to litigations, including collection actions, lien assessments, and an SEC lawsuit alleging securities fraud. The debtors filed for bankruptcy to sell their assets and intend to prepare the assets for sale and hire an investment banker in the next month. The company proposes a sale timeline that will conclude at the beginning of December this year.

Luca seeks approval of a $2 million revolving DIP financing facility from Schumann/Steier Holdings.

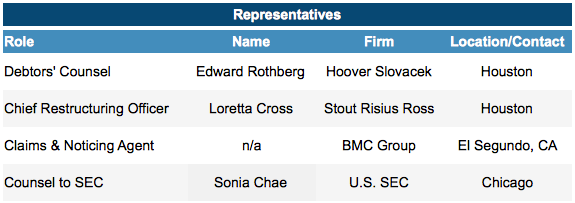

The debtors have hired Hoover Slovacek in Houston as counsel, BMC Group as claims agent, and Loretta Cross of Stout Risius Ross as chief restructuring officer.

BackgroundLuca was founded in 2005 and is wholly owned by Bingqing Yang, who financed the company with investment from China and Japan.

Luca’s primary assets are located in Iberville Parish and Ascension Parish, La., and consist of three operating oil and gas wells, a water disposal well and a shut-in oil and gas well. The company also owns oil and gas leases in Texas and working interests in various locations. A recent report states that

Luca has proven reserves of 3.2 billion cubic feet of gas and 450 million barrels of oil. The debtors employ six people.

In July 2015, the SEC sued several

Luca entities in the U.S. District Court for the Northern District of California, alleging that

Luca investor funds were not spent in accordance with the entities’ fundraising documents (Case no. 15-03101). The

complaint alleges that the company targeted the Chinese-American community and Asian investors in unregistered securities offerings. The SEC further alleges that Yang used company funds for personal expenses. The SEC has moved to appoint a receiver.

The debtors did not include a list of creditors in its filings.

Debt Structure / DIP Financing MotionThe company’s prepetition capital structure includes:

- Secured debt: In excess of $500,000 of liens have been placed against the company’s Belle Grove #1 well in Louisiana. The Cross affidavit discloses that in addition to investor money, “there may be significant loans” made to the debtors. Cross says that the company is obtaining the documentation for the loans, which may be related to investor funds or insider funds that were invested in one entity and later loaned to another entity.

- Unsecured debt: More than $10 million in unsecured debt, including accounts payable of about $2.1 million, and amounts owed to critical vendors of about $317,000.

The debtors seek approval of a revolving DIP credit facility with Schumann/Steier Holdings or its designee up to $2 million (with a $200,000 interim draw) pursuant to a

budget, subject to a 10% variance. The DIP proceeds will be used to cover projected shortfalls in operating expenses and professional fees. The DIP financing is pursuant to a

credit term sheet attached as Exhibit B to the motion.

Luca says that it has insufficient cash to conduct ordinary course operations, and that the financing is needed to pay for, among other things, ordinary course saltwater removal to resume production in one of its wells.

The loan bears an interest rate of LIBOR + 15%, with a LIBOR floor of 3% (after the interim draw, interest will accrue on the greater of the outstanding DIP balance or $1 million). The financing also includes (a) a commitment fee of 2.5%, (b) a collateral monitoring fee of $11,000 per month, and (c) an initial advance of $30,000 for reimbursement of due diligence expenses.

Upon final approval of the DIP facility, the first subsequent draw will be for $800,000, and subsequent draws will be in increments of at least $250,000 and subject to proved reserves of the debtors’ interest in mineral interests (omitting third party interests) in excess of $4 million of which at least $2.5 million are proved developed producing reserves.

The DIP financing terminates nine months from interim approval.

The DIP financing will be secured by priming liens on substantially all of the debtors’ assets, and will also have superpriority administrative expense status.

The proposed financing also provides that the debtors may not seek to confirm a plan unless it pays the DIP financing in full. Sale proceeds will be applied first to payment of outstanding amounts under the DIP financing.

The proposed financing also contains the following milestones relating to the sale process:

- Investment banker retention: motion filed by Aug. 21 (15 days from the petition date)

- Bid procedures motion: filed by the earlier of (a) 30 days after filing of motion to retain investment banker, or (b) 45 days after the petition date

- Bid deadline: Dec. 4 (120 days from date of filing of motion to retain investment banker)

- Auction: Dec. 7 (121 days from date of filing of motion to retain investment banker/broker)

- Closing date: as soon as practical after court approval, with payment of all DIP facility amounts at closing

The DIP financing also provides that Schumann/Steier Holdings may credit bid.

Critical Vendor MotionThe company seeks to pay its critical vendors that delivered materials, supplies, goods, products and related items before the filing up to about $214,000, about 68% of the $317,000 prepetition amount owed to these creditors. The debtors also seek to condition payment on customary trade terms. The identities of the critical vendors were disclosed in

Exhibit A to the motion.

Other MotionsIn addition to the motions described above, the debtors also filed various standard first day motions, including the following:

A hearing on the motions has not been scheduled yet.